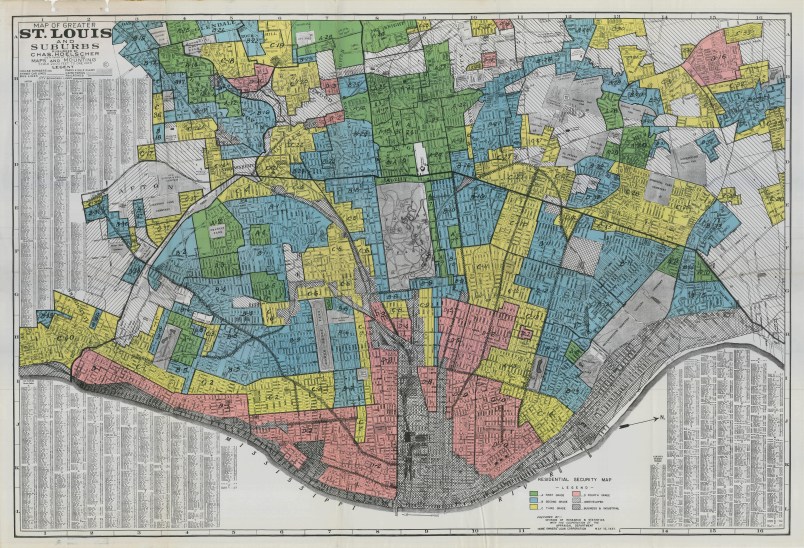

Redlining refers to the practice of mortgage lenders denying whole communities access to credit on the basis of race, usually blackness. During the Great Depression, real estate developers, housing officials, economists, bankers, and urban planners built an elaborate federal bureaucracy meant to resuscitate the American economy by catering to the perceived wants and needs of white homebuyers. White housing officials practiced their racism largely behind closed doors or through bureaucratic back channels at government agencies such as the Home Owners’ Loan Corporation and the Federal Housing Administration (FHA). Discrimination in housing was not yet illegal. Still, explicitly separating the races – especially though housing – ran the risk of violating the property rights and civil rights provisions outlined in the Fifth and Fourteenth Amendments. Redlining thus required a measure of discretion.

The pervasiveness of redlining forced African Americans and other people of color to rent from landlords, often at exorbitant prices, or to take out more dangerous forms of credit if they hoped to buy a home. As early as 1934, black borrowers across the country complained to the black press and to civil rights groups of being turned away from federally insured banks and government offices. A general lack of transparency about home finance and within the government housing apparatus, however, made it difficult to discern a national trend.

This June 1938 letter helped break the redlining story.

Sent by Roy Wilkins, assistant head of the NAACP, to Robert Weaver, a high-ranking black appointee at the Department of the Interior, the letter describes Wilkins receiving “a telephone message a few days ago from a young white friend of ours in Brooklyn who said he was employed in some capacity with the Federal Housing Administration.” The white staffer was, in effect, a whistleblower looking to hasten the illegality of Jim Crow housing. He revealed, by Wilkins’s telling, that “Unofficially, the FHA is making as one of its requirements for guaranteeing mortgages that the builders insert…[a]deed…clause prohibiting sale, rental, or occupancy by persons of African descent.” In subsequent correspondence, even Robert Weaver, with his top-tier connections in Washington, would admit to having no knowledge of what the FHA was doing.

No doubt wishing to protect his source’s identity, Wilkins does not give his contact’s name. Nor does he send the letter to Weaver’s work address, fearing interception. Instead, he uses the correspondence to begin rallying activists to attack the practices about which isolated black buyers had long been complaining. In short order, Thurgood Marshall, Walter White, and other activists pressured Washington to make public the FHA’s Underwriting Manual and its discriminatory guidelines. By the end of 1938, the black press, as this passage from the Los Angeles Sentinel captures, had geared up for a national fight: “Americans who have been protesting Hitler’s despicable plan to herd German Jews into ghettoes will be surprised to learn that their own government has been busily planning ghettos for American Negroes through the Federal Housing Authority [sic].”

Federal redlining has, today, become a signature piece of almost any discussion of racial discrimination and the wealth gap in modern America. But prior to a leak from a white ally in Brooklyn, the practice could be dismissed as mere rumor among a jilted class of African Americans homebuyers. Wilkins’s whistleblower insisted “that we would not be able to get anything except denials if we approached this matter directly through official channels.” That proved true for another thirty years. Following decades of organizing, litigation, and the losses of countless lives, the federal government finally made explicit housing segregation illegal with the 1968 Fair Housing Act. One well placed phone call, placed a generation earlier, made a huge difference.

“Primary Source” is already better than “The Slice”.

I like it.

“The pervasiveness of redlining forced African Americans and other people of color to rent from landlords, often at exorbitant prices”

Rather than stroll down memory lane and smile that, wow, redlining is now illegal, I’d much prefer a story about the here and now. Wake up. 21st century redlining is alive and well.

Yup, we’ve moved very slowly. Now, at least, if you can prove redlining, you can get recompense. Back then, nothing. One of the “innovations” of the financial industry in the past generation has been to make redlining “objective”. If you steer black people to more expensive loans and credit agreements than white people of the same income level, then they’ll be more likely to default, or to have trouble paying their other bills, because, hey, less available income and less savings. And then you can point to that increased likelihood of default as a reason for steering them to more expensive loans.

Very nice start to History. Brief, interesting and something I could post to Facebook to get TPM a few more clicks (and hopefully readers).

That is one huge ‘if.’ And it’s not just in housing, either.

Banks, credit card companies and insurers can now use your social media data to determine the terms by which they’ll do business with you.