Donna received the letter canceling her insurance plan on Sept. 16. Her insurance company, LifeWise of Washington, told her that they’d identified a new plan for her. If she did nothing, she’d be covered.

A 56-year-old Seattle resident with a 57-year-old husband and 15-year-old daughter, Donna had been looking forward to the savings that the Affordable Care Act had to offer.

But that’s not what she found. Instead, she’d be paying an additional $300 a month for coverage. The letter made no mention of the health insurance marketplace that would soon open in Washington, where she could shop for competitive plans, and only an oblique reference to financial help that she might qualify for, if she made the effort to call and find out.

Otherwise, she’d be automatically rolled over to a new plan — and, as the letter said, “If you’re happy with this plan, do nothing.”

If Donna had done nothing, she would have ended up spending about $1,000 more a month for insurance than she will now that she went to the marketplace, picked the best plan for her family and accessed tax credits at the heart of the health care reform law.

“The info that we were sent by LifeWise was totally bogus. Why the heck did they try to screw us?” Donna said. “People who are afraid of the ACA should be much more afraid of the insurance companies who will exploit their fear and end up overcharging them.”

Donna is not alone.

Across the country, insurance companies have sent misleading letters to consumers, trying to lock them into the companies’ own, sometimes more expensive health insurance plans rather than let them shop for insurance and tax credits on the Obamacare marketplaces — which could lead to people like Donna spending thousands more for insurance than the law intended. In some cases, mentions of the marketplace in those letters are relegated to a mere footnote, which can be easily overlooked.

The extreme lengths to which some insurance companies are going to hold on to existing customers at higher price, as the Affordable Care Act fundamentally re-orders the individual insurance market, has caught the attention of state insurance regulators.

The insurance companies argue that it’s simply capitalism at work. But regulators don’t see it that way. By warning customers that their health insurance plans are being canceled as a result of Obamacare and urging them to secure new insurance plans before the Obamacare launched on Oct. 1, these insurers put their customers at risk of enrolling in plans that were not as good or as affordable as what they could buy on the marketplaces.

TPM has confirmed two specific examples where companies contacted their customers prior to the marketplace’s Oct. 1 opening and pushed them to renew their health coverage at a higher price than they would pay through the marketplace. State regulators identified the schemes, but they weren’t necessarily able to stop them.

It’s not yet clear how widespread this practice became in the months leading up to the marketplace’s opening — or how many Americans will end up paying more than they should be for health coverage. But misleading letters have been sent out in at least four states across the country, and one offending carrier, Humana, is a company with a national reach.

“If you’re an insurance company, you’re trying to hang onto the consumers you have at the highest price you can get them,” Laura Etherton, a health policy analyst at the U.S. Public Interest Research Group, told TPM. “You can take advantage of the confusion about what people get to have now. It’s a new world. It’s disappointing that insurance companies are sending confusing letters to consumers to take advantage of that confusion. The reality is that this could do real harm.”

_____

Before Obamacare, Donna paid a $724 monthly premium for $10,000 deductible, catastrophic health coverage from LifeWise, a subsidiary of the state’s Blue Cross/Blue Shield affiliate. She asked that TPM withhold her last name because she was disclosing personal financial information.

The Sept. 16 letter from LifeWise told her that her existing plan was being canceled to comply with the new requirements of Obamacare and that she would automatically be rolled over into a new plan that was the “closest match” to her old plan. “If we don’t hear from you, we’ll automatically move you to this plan and you’ll be covered starting January 1, 2014,” the notice read.

Under the new LifeWise plan, Donna would have to pay more than $1,000 a month, a nearly $300 per month increase and a huge hit for a family with an income around $40,000. It was bare-bones coverage by ACA standards, with a $6,350 deductible.

The letter, which you can read here, made no mention of the insurance marketplace that was about to open, where she could shop around for other options. It did mention that she might qualify for financial help in the form of a tax credit but the onus was on Donna to call the insurer for more information.

Fast forward a month, and Donna was able to log onto Washington’s marketplace and shop for insurance. And what did she find? Options. A LifeWise plan with the same deductible they offered her outside the exchange was a little cheaper. Plans with a lower deductible had the same or lower premiums as the LifeWise plan. What she ended up buying was a plan through Community Health Plan of Washington with a $250 deductible.

And crucially, she also discovered she would qualify for a federal tax subsidy that would knock her monthly premium to $80. Her daughter could enroll in Medicaid, at no cost to the family.

So here’s the bottom line: If Donna had taken the default option that LifeWise offered outside of the marketplace, she would have paid nearly $1,000 more per month for a worse plan than she was able to obtain on the marketplace.

A LifeWise spokesman told TPM that the Washington marketplace had done plenty of its own advertising and the company assumes that customers know they have other options. He also noted that more information was available on the company’s website.

“Our experience is that our customers are already aware that they have other options in the market and that we’ve never had to tell them in the past that we have competitors,” Eric Earling, director of corporate communications at Premera Blue Cross/Blue Shield, said. “We knew that (the marketplace) would have a robust marketing campaign for themselves and knew they didn’t need any additional help from us.”

As a result of the letter LifeWise sent to Donna and other customers, state regulators in Washington issued a consumer alert on Sept. 19, warning residents about the misleading information. “Don’t just take what your insurance company says, make sure you shop around. You have the right to buy any plan inside the new exchange or in the outside market,” Insurance Commissioner Mike Kreidler said in the alert.

But the agency doesn’t have the statutory authority to stop LifeWise from sending the misleading letters, a spokeswoman told TPM. The company controls one-third of the state’s 300,000-person individual health insurance market — leaving a lot of people at risk of being duped.

“Yes, that’s possible,” Stephanie Marquis, the spokeswoman, said when asked if some Washingtonians could be paying much more for insurance than they could if they went on the exchange because of LifeWise’s actions.

“One of our concerns has been that people don’t know they have these new rights,” Marquis said. “The insurance companies can manipulate or withhold that information to increase their market share. It’s just really disingenuous.”

_____

Donna’s experience isn’t an isolated incident, however. And the wider spread the issue is, the likelier it becomes that some people have been manipulated into spending more for insurance than they should.

Kentucky fined Louisville-based Humana for sending out letters with similarly misleading information to customers in that state. They received complaints about an Aug. 21 letter that pressed customers to renew their policy now or risk increased rates under Obamacare.

Kentucky fined Louisville-based Humana for sending out letters with similarly misleading information to customers in that state. They received complaints about an Aug. 21 letter that pressed customers to renew their policy now or risk increased rates under Obamacare.

But like LifeWise, Humana downplayed the fact that people could search the marketplace for other insurance options or that they might qualify for Obamacare’s financial assistance, state insurance commissioner Sharon Clark, pictured, told TPM in an interview. A footnote referenced the “open enrollment period” that started Oct. 1. Humana directed customers to their website for more information about the marketplace, but offered no further explanation.

After receiving the letter, which you can read here, some customers were badgered through phone calls to make a decision, Clark said. Of the 6,500 people who received a letter, 2,200 actually responded and gave the company their answer before they had a chance to look at what the Kentucky marketplace had to offer.

But Clark’s office soon stepped in. They fined Humana $65,000 for the “misleading” information, and the 2,200 respondents were released from their obligation to Humana and freed to shop for insurance through the Obamacare marketplace starting Oct. 1.

The most troubling part of the Humana case is that the company was pushing customers into a Humana insurance plan that was more expensive than the plan Humana was selling on the Obamacare marketplace, without the financial help available under Obamcare.

Clark gave the example of a single mother with children who was urged to sign up for a Humana plan with a monthly premium of $719.86. That price is higher than any comparable plan for sale on the state’s insurance marketplace, Clark said — not to mention that the mother might have qualified for tax subsidies to help pay for it if she went through the marketplace, as Donna did.

“People don’t think about insurance every day,” Clark said, “and in an environment with so many changes, this has been a period of confusion and uncertainty for people.”

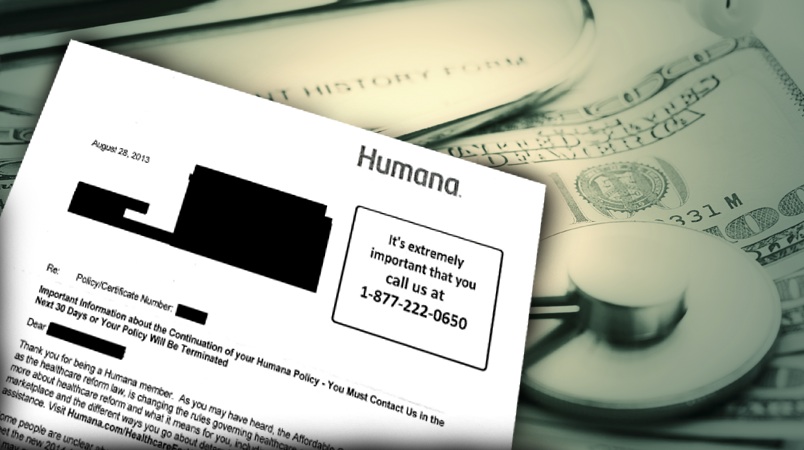

Colorado regulators also received complaints about a similar Humana letter, dated Aug. 28 on a copy obtained by TPM, that went out to 3,400 customers in their state.

It explained options available on the Obamacare marketplace and financial help in, again, a footnote. The company wasn’t fined as it was in Kentucky, but state officials forced Humana to send out an apology and a corrected letter that met the state’s standards.

“The letter appeared threatening,” Vincent Plymell, a spokesman for the state insurance department, told TPM. “You’ve got to let people know their options. You can’t make it seem like they have to stick with your company.”

State officials in Missouri also told TPM that they have received complaints about misleading letters from Humana and were in the process of investigating them.

Asked by TPM about the Kentucky letter that resulted in a fine, Humana senior vice president for corporate communications Tom Noland offered the following statement via email, but declined to comment further.

“In retrospect, the letter could have been more consumer-friendly and we’ve rewritten it with that in mind. We are continuing to work closely with the Department of Insurance to ensure our messaging is clear and not adding confusion to consumers during this period of adjustment and transition.”

Clark, the Kentucky insurance commissioner, told TPM that Humana executives had told state officials that there had been “a major disconnect” between the marketing and government compliance arms of the company.

“That was the excuse they gave us,” she said. “That was the rationale.”

“This is a great example of the kind of consumer abuses that are typical of the insurance industry, and they’re supposed to stop under the ACA,” Ethan Rome, executive director of Health Care For America Now, a pro-Obamacare advocacy group, told TPM. “In this case, they’re trying to get in just one more abuse.”